In 2026, business debt consolidation has become a crucial tool for small and mid-sized companies aiming to simplify finances, reduce monthly payments, and regain control over cash flow. Yet while consolidation can be a lifeline, not all businesses succeed in using it effectively. Understanding why debt consolidation fails and how to qualify the right way can make the difference between financial stability and continued financial pressure.

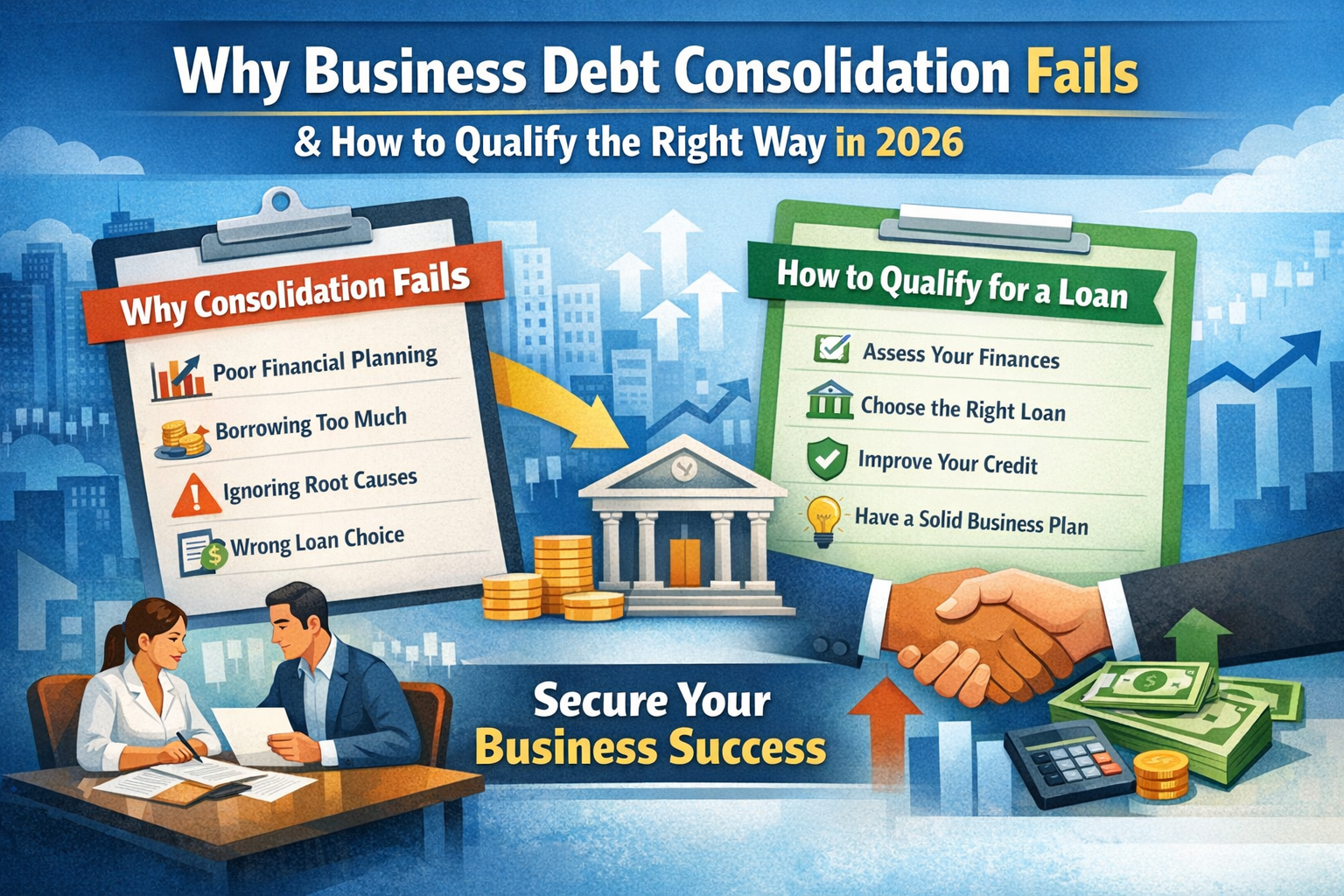

Why Business Debt Consolidation Fails for Some Companies

1. Failing to Assess True Financial Health

Many businesses approach debt consolidation without a clear understanding of their overall financial situation. They often focus only on monthly payments instead of analyzing total debt, interest rates, and cash flow trends. Without accurate bookkeeping and a realistic financial plan, a new consolidation loan may simply hide deeper financial problems rather than solve them.

2. Borrowing More Than Necessary

Some business owners consolidate existing debt and take additional funding at the same time “just in case.” This approach can increase monthly obligations and extend repayment periods. Instead of reducing financial pressure, it can create a larger debt burden over time.

3. Ignoring the Root Cause of Debt

Debt consolidation solves the symptoms, not the underlying cause. Businesses that continue overspending, struggle with receivables, or ignore operational inefficiencies may end up facing the same financial challenges again even after consolidating their debts.

4. Choosing the Wrong Loan Program

Not every consolidation loan fits every business model. Some programs include hidden fees, shorter repayment terms, or variable interest rates that create unexpected financial strain. Selecting a loan without considering revenue patterns, business size, or industry type is a common reason consolidation fails.

5. Poor Planning and Cash Flow Management

Successful consolidation requires consistent repayment planning. Businesses that fail to prepare for seasonal fluctuations, unexpected expenses, or inconsistent cash flow may struggle to repay the new loan. This can lead to missed payments and even worse credit outcomes.

How to Qualify the Right Way for a Consolidation Loan

1. Evaluate Your Business Finances First

Before applying for business debt consolidation, review all existing debts, interest rates, and monthly payment obligations. Identify high-interest loans that should be included in the consolidation plan. Knowing your financial numbers strengthens your application and ensures the new loan truly benefits your business.

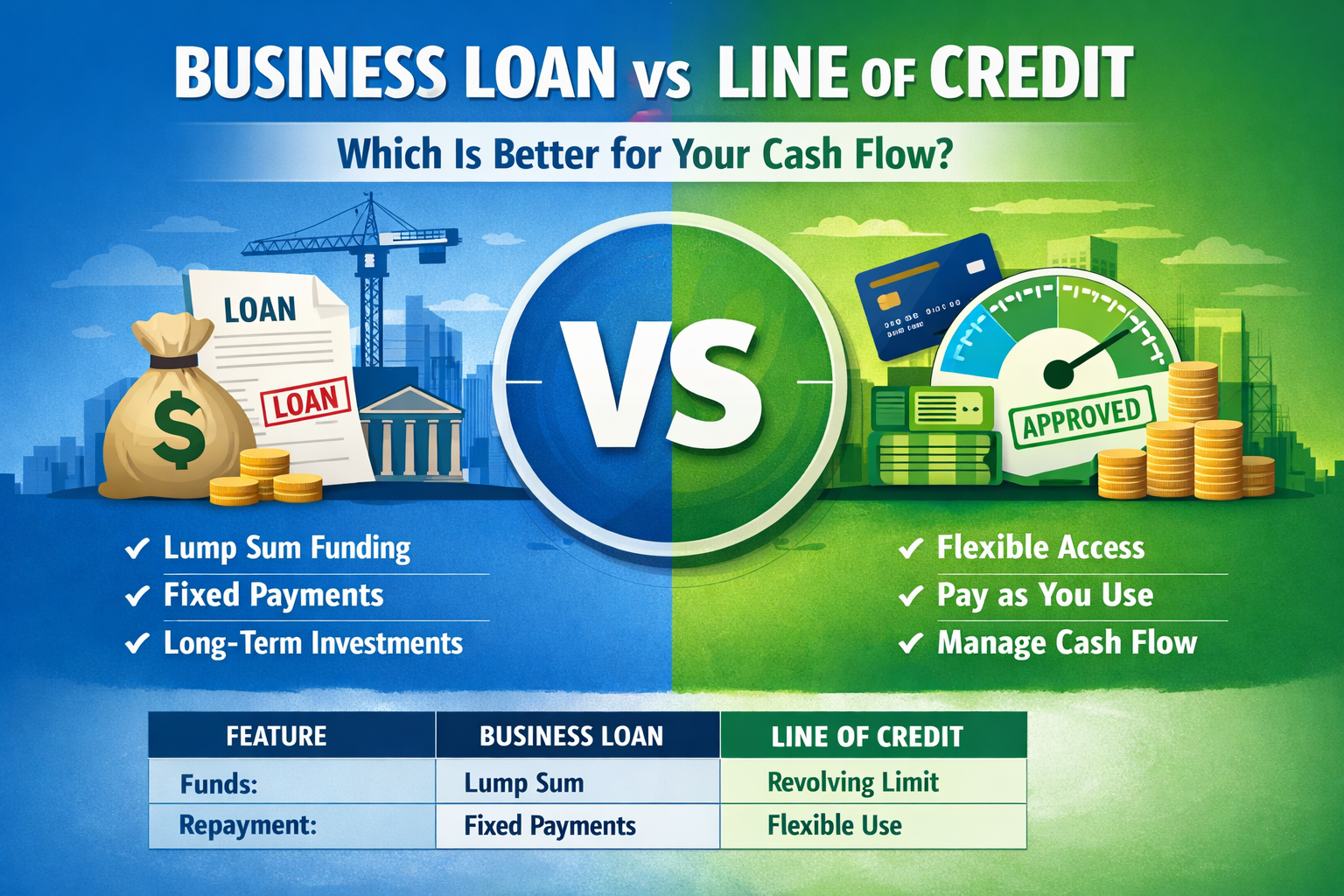

2. Choose the Right Type of Consolidation Loan

Businesses in 2026 have several consolidation options, including:

Traditional Term Loans: Fixed monthly payments and predictable repayment schedules.

SBA-Backed Consolidation Loans: Lower interest rates and longer repayment terms for eligible businesses.

Merchant Cash Advance (MCA) Consolidation: Flexible repayment based on daily sales for businesses with fluctuating revenue.

Choosing a loan structure that matches your cash flow and growth strategy is essential.

3. Maintain a Healthy Credit Profile

Some lenders offer consolidation loans for businesses with lower credit scores, but a strong credit profile still improves approval chances and secures better interest rates. Even small improvements, such as reducing overdue payments or maintaining active credit lines, can strengthen your eligibility.

4. Prepare a Clear Business Plan

Lenders want evidence that consolidation will improve financial stability. A clear plan outlining cash flow management, debt repayment strategy, and expected business growth shows responsibility and increases approval likelihood.

5. Work with Trusted Lenders

Choose lenders who specialize in supporting small businesses and offer transparent loan terms. Working with experienced lenders who evaluate overall business performance instead of relying only on credit scores can help businesses secure consolidation loans that truly support long-term growth.

Tips for Successful Debt Consolidation

Stick to a Budget: Ensure your monthly repayment plan is sustainable.

Avoid New Debt: Don’t accumulate more debt during consolidation.

Monitor Progress: Track your debt reduction and financial performance.

Leverage Expertise: Work with financial advisors or lending specialists to select the most suitable loan type.

Conclusion

Business debt consolidation can be a powerful tool when approached strategically. Many companies fail because they skip financial assessment, choose unsuitable loan programs, or continue the habits that caused debt in the first place. By evaluating your finances, choosing the right program, preparing a solid business plan, and working with trusted lenders, your business can consolidate debt successfully, improve cash flow, and focus on growth.

CTA: Ready to take control of your business debt? Apply for a consolidation loan today and simplify your payments with fast approvals, flexible terms, and support tailored for your business.